The Growing Call for Lifetime Income Products in Australia

We welcome the Grattan Institute’s recent report, Simpler Super: Taking the Stress Out of Retirement, highlighting the urgent need to improve access to lifetime income products for Australian retirees. While we agree with the report’s diagnosis of the challenges facing Australia’s retirement income system, we do not agree with all of its proposed solutions. Some recommendations align with our views, but others require careful consideration to avoid unintended consequences.

The Diagnosis

The report identifies excessive complexity in Australia’s superannuation system, leaving many retirees anxious and hesitant to spend their savings. Around 80% of Australians find retirement planning complicated, and 60% anticipate financial stress in retirement. As a result, many retirees avoid drawing down their superannuation balances, effectively turning the system into an inheritance scheme rather than a retirement income source.

This issue is not new. In 2014, the Financial System Inquiry Final Report (Murray Review) raised concerns about retirees’ ability to manage longevity risk in the drawdown phase. Similarly, in 2022, Optimum Pensions surveyed industry professionals about the biggest challenge facing superannuation. Most responses aligned with the Grattan Institute’s findings—we need to address the retirement phase of the system.

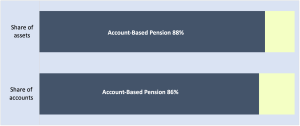

The core problem is clear: almost all retirees rely on account-based pensions (see Chart 1). The Grattan Institute posits that this is because such pensions are “effectively what the system pre-selects for them”. It is undoubtedly the only retirement income product most superannuation funds offer.

Chart 1: Account-based pension share of retirement super (2023)

Source: Grattan Institute, Simpler Super: Taking the Stress Out of Retirement, 2025

Why is this a problem?

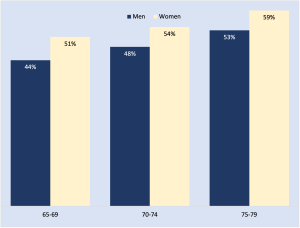

Account-based pensions do not provide longevity protection. Account-based pensions are subject to minimum drawdown rules. The Grattan Institute report that about half of retirees draw on their super at the minimum required drawdown rates (see Chart 2).

The predominance of minimum drawdown rules leads to retirees withdrawing too cautiously, either because they mistakenly believe the minimum rate is a recommended rate or due to a fear of running out of money. Either way, this results in lower retirement spending than necessary, ultimately reducing retirees’ quality of life.

Chart 2: Share of account-based pensions being drawn at the minimum, by age and gender (2019)

Source: Grattan Institute, Simpler Super: Taking the Stress Out of Retirement, 2025

The 2024 Mercer Global Pension Index reinforces this diagnosis. Seven of the top eight countries in the index prioritise retirement income streams. Australia is the odd one out (See Table 1).

Table 1: 2024 Mercer Global Pension Index Top Eight

| Country | Grade | Retirement benefit requirements |

| Netherlands | A | Lifetime pensions with a limit of 10% of the benefit taken as a lump sum |

| Iceland | A | Lifetime annuities required for most mandatory contributions |

| Denmark | A | Benefit options available but significant contribution limits exist for lump sum plans |

| Israel | A | Lifetime annuities although they are not guaranteed |

| Singapore | B + | Lifetime annuities with three indexation options |

| Australia | B + | None |

| Finland | B + | Lifetime indexed pensions with no lump sums available |

| Norway | B + | The annuity must be payable for at least 10 years and until age 77 |

Source: Mercer, Simplifying super to get the best retirement outcomes, 2024

The evidence is clear: if Australia is to join the world’s best retirement systems, it must shift its focus from accumulation to sustainable retirement income.

The Prescription

The Grattan Institute’s key recommendation is to increase the availability and usage of lifetime income products to provide Australians with an income for life. Their proposals include:

1. A Default with an Opt-Out Option

The Grattan Institute suggests a default mechanism where retirees would automatically allocate 80% of their superannuation balance (above $250,000) to a lifetime income product, with the option to opt out.

We support this approach. A default with an opt-out option leverages behavioural finance principles to improve retirement outcomes while preserving choice. It addresses common behavioural biases that lead retirees to underutilise their savings, ensuring they receive the benefits of longevity protection.

Optimum Pensions’ submission to the 2023 Treasury Discussion Paper Retirement phase of superannuation proposed a similar approach—allocating a portion of retirement savings to lifetime income streams, commencing at age 72, while allowing members to opt out.

Retirees can benefit significantly from allocating a proportion of their superannuation balances to a lifetime income product, such as a lifetime annuity or investment-linked annuity. The Grattan Institute modelled the impact of allocating a proportion of superannuation balance to retirement incomes for different balances. Table 2 shows results for a simple lifetime annuity, while previous modelling by Optimum Pensions shows that choosing an investment-linked annuity can boost retirement income by between 15% – 30% when compared to traditional life annuities and account-based pensions.

Table 2: Boost total retirement incomes from annuitising a share of the superannuation balance

| Super Balance | Single | Couple | ||

| Allocation | Increase | Allocation | Increase | |

| $250k | 0% | +0% | 0% | +0% |

| $375k | 27% | +1% | 27% | +1% |

| $500k | 40% | +1% | 40% | +1% |

| $625k | 48% | +7% | 48% | +7% |

| $750k | 53% | +13% | 53% | +13% |

| $875k | 57% | +19% | 57% | +19% |

| $1m | 60% | +26% | 60% | +26% |

Source: Grattan Institute, Simpler Super: Taking the Stress Out of Retirement, 2025

Another benefit to retirees from allocating some of the superannuation balance to a lifetime income product is the favourable treatment of annuities in the Age Pension means test: only 60% of their value counts toward the means tests, meaning retirees can receive higher Age Pension payments. Optimum Pensions modelling shows that means-tested Age Pensioners can get up to $32,000 a year more from Centrelink just by using a lifetime income product.

Other benefits of lifetime income products include:

- Increased happiness—knowing there is a secure income for life.

- Increased spending power—as retirees feel more confident using their money.

- Better budgeting—since income is predictable.

- Protection against scammers—who often prey on retirees worried about running out of money.

We agree with the Grattan Institute that a range of lifetime income products should be available to retirees.

However, successful implementation requires careful consideration:

- Education & Communication: Retirees need clear information on how the default works and the benefits of lifetime income products.

- Well-Designed Products: Default solutions must be flexible, cost-effective, and tailored to retiree needs.

- Simple Opt-Out Process: Retirees should be able to opt out easily if the default doesn’t suit them.

2. The Case Against Government-Issued Annuities

This might be the most controversial recommendation. While the Australian financial services industry has faced challenges in establishing an efficient market for lifetime income products at scale, progress is being made and more retirees than ever now have access to lifetime income products. According to Retirement Edge, as of December 2024, five superannuation funds, five platforms, and three life insurers offer lifetime income products and new offerings expected in 2025.

Would the adoption of lifetime income products grow faster if the government stepped in? We doubt it. A government-run annuity would not necessarily simplify the system or reduce complexity. It could also crowd out private-sector innovation, leading to fewer choices for retirees.

Some may argue that government-issued annuities would ensure affordability and accessibility. However, the real issue is not a lack of annuity products but a lack of awareness and uptake. The priority should be removing regulatory barriers and improving consumer education and guidance rather than introducing a government-run solution.

The Grattan Institute recommends guiding retirees to a “simple lifetime annuity”. This recommendation minimises the broad range of retirees’ needs and preferences. The most suitable type of annuity for a particular retiree will depend on their individual circumstances and risk tolerance. In fact, the report agrees that retirees could benefit over time from a range of annuity options.

The report highlights that retirees with an investment-linked annuity can benefit from continued access to the equity risk premium during retirement, leading to higher retirement incomes over time.

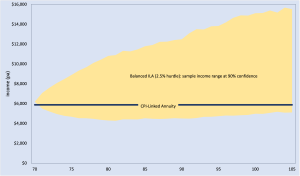

Chart 3 compares the income from a CPI-linked annuity and an investment-linked annuity for a 70-year-old male. The CPI-linked annuity provides a consistent real income stream, represented by the dark horizontal line [1], which maintains purchasing power throughout retirement.

In contrast, the investment-linked annuity offers exposure to growth assets while still guaranteeing a lifetime income. Our modelling indicates a 90% confidence interval for potential income outcomes, shown by the yellow-shaded region [2]. This structure allows retirees to capture equity risk premium during their retirement phase, potentially leading to significantly higher real incomes, particularly in later years.

Chart 3: CPI-Linked vs Investment-Linked Annuity Income (ILA) Comparison (today’s purchasing power)

Source: Optimum Pensions modelling [3]

Source: Optimum Pensions modelling [3]

Table 3 compares their key features. As discussed below, many investment-linked annuities available in Australia allow retirees to cater to their specific risk tolerance and stability preferences by selecting an appropriate investment mix. The retiree can also change this mix as circumstances change.

Table 3: CPI-linked annuities versus investment-linked annuities

| Feature | CPI-linked annuity | Investment-linked annuity |

| Income payments | Adjusted in line with CPI | Linked to investment performance |

| Potential for returns | Lower | Higher |

| Risk | Lower | Higher |

| Stability | Higher | Lower |

Shouldn’t all retirees be guided to the most suitable products rather than just the simplest if it leads to better retirement outcomes?

The Grattan Institute suggests that annuities are typically ‘one-shot games’. Once purchased, a retiree has the product for life, even if there is a better option in the future. The thing with lifetime income products is that there is no perfect product. What is most important is that the retiree does not purchase an unsuitable product.

The inability to switch products might be a significant problem for traditional lifetime annuities but less so for the new breed of investment-linked annuities. Many of these products allow for a much more extended cooling-off period than the 14 days required by legislation—for some, it is up to six months. These products also allow retirees to choose an investment option or options and even switch between options as their circumstances change.

The Grattan Institute’s report argues that “Government-provided annuities are the best option” but does not adequately explain why this helps retirees who want to switch to a “better option in the future”. Whether the annuity is issued by the government or the private sector, the retiree will still be unable to do so.

The Grattan Institute also refers to the ‘annuity puzzle‘, that is, the disconnect between economic theory, which suggests that purchasing annuities is a financially sound decision for retirees, and the reality that very few people choose to annuitise their retirement savings. Many of the reasons proposed for this puzzle will not be addressed by the government becoming the provider of annuities.

3. Better Guidance for Retirees

Yes—Australians need better guidance to plan their retirements. The Grattan Institute points out that leaving retirees to manage this complexity themselves is expecting each retiree to “become an actuary”!

A government guidance service, as proposed by the Grattan Institute, is a worthwhile recommendation; we support this initiative, particularly if it enhances rather than duplicates existing advice and guidance provided by superannuation funds, financial advisers, and financial services institutions. Including interactive tools to act as an independent source of information and guidance would be a minimum requirement.

However, this service should not minimise the role of the financial services industry. If trust in the industry is an issue, as the Grattan Institute suggests, then the industry must confront this and work to mitigate the problem. The superannuation fund will always be an important intermediary between a consumer and the retirement income system.

We should ask how much of this trust deficit is due to, among other things, the dilemma facing trustees who are caught between their desire to provide adequate support to their members and the strict advice regulations that restrict how much support they can provide.

A key challenge is the lack of regulatory clarity around guidance versus advice. Superannuation funds are restricted in how much information they can provide without it being classified as financial advice. There is an urgent need for a regulatory framework that allows funds to offer more structured guidance to retirees without stepping into full advisory services.

The financial services industry is waiting for the government’s Delivering Better Financial Outcomes (DBFO) reforms, which aim to improve the quality and accessibility of financial advice. In the meantime, there are actions superannuation fund trustees can take.

The Grattan Institute correctly points out the importance of how choices are described and presented. That is, how they are framed. Superannuation funds could consider changing the language they use when discussing these choices with their members. Lifetime income products are forms of insurance.

Research from the Centre of Excellence in Population Ageing Research indicates that providing retirement income projections to superannuation fund members can significantly improve their understanding of their retirement savings and encourage them to make more informed decisions about their retirement planning. How many superannuation funds include retirement income projections on annual statements or with benefit quotes?

When helping members with their retirement planning, we would do well to heed the advice of Moshe Milevsky, Professor of Finance at York University and widely acknowledged global annuity guru, to “balance emotion and math.”

4. Ensuring Superannuation Funds Deliver for Retirees

We support greater accountability for superannuation funds in developing and reporting on their retirement income strategies. However, we do not favour the Grattan Institute’s proposed Top 10 approach. In 2018, the Productivity Commission recommended a similar best-in-show model with a shortlist of 10 superannuation funds to replace the current default fund system. If the goal is to limit harm from underperforming funds, why restrict the list to 10?

A more effective alternative might be the Conexus Institute’s proposed retirement licensing regime, which aims to improve the quality and consistency of retirement services offered by superannuation funds. This approach could ensure that all funds meet a high standard rather than arbitrarily limiting choice.

Conclusion: The Time to Act is Now

Optimum Pensions agrees with the Grattan Institute’s objective of reducing retiree stress and promoting the effective use of retirement savings. Many of its recommendations align with industry concerns, and we support its call for increased adoption of lifetime income products.

We echo the call from David Bell and Geoff Warren to engage with the report rather than dismiss it outright. However, if the industry does not want to see a future where government intervention reshapes the retirement landscape, it must take the lead in designing and delivering effective retirement solutions.

We also invite ASFA and SMC to share their perspectives. What are their positions on providing lifetime income solutions? How are they guiding the industry to fulfil the promise of superannuation for all Australians in retirement? The regulators have issued unambiguous warnings—inaction is not an option.

David Orford founded Optimum Pensions in 2017 to help the superannuation industry develop innovative longevity retirement solutions. At the time, he said that lifetime income streams would be crucial in achieving this goal. His vision is to see Australia’s superannuation system become a world-class retirement system. With increasing recognition from government, regulators, and industry, that vision is now within reach.

[1] Based on rates from Challenger Life accessed on 21 February 2025 [2] Based on rates from Generation Life obtained on 21 February 2025, the product features a 2.5% LifeBooster option that allows you to receive more income in the earlier years of retirement. We assumed a 1% fee plus a 0.35% longevity protection provision. [3] Full details of the modelling available on request.