Treasury’s Best Practice Principles: A Roadmap for Better Retirement Outcomes

The Australian superannuation industry stands at a critical juncture. With over 2.5 million Australians expected to transition into retirement over the next decade, the need for high-quality retirement income solutions has never been more pressing. Treasury’s recently released consultation paper, “Guidance on best practice principles for superannuation retirement income solutions,” provides a clear framework for trustees to lift the bar on retirement outcomes.

The Shift from Accumulation to Income

For decades, Australia’s superannuation system has excelled at helping members grow their retirement savings. However, the retirement phase tells a different story. Many retirees are drawing down conservatively, dying with significant balances intact, and not maximising their living standards throughout retirement. This behaviour conflicts with the legislated objective of superannuation: to deliver income for a dignified retirement.

Treasury’s best practice principles acknowledge that one product alone cannot balance the three key objectives of the Retirement Income Covenant. Members need solutions that simultaneously maximise income, manage risks (including longevity, sequencing and inflation risks), and maintain flexible access to capital.

The Critical Role of Lifetime Income Products

A cornerstone of Treasury’s principles is the inclusion of lifetime income products in retirement solutions. Principle 5 explicitly states that trustees should provide members with access to a lifetime income product that is not the Age Pension. More significantly, Principle 9 calls for trustees to construct at least one retirement income solution that includes a lifetime income product component, with regard to likely Age Pension eligibility.

Research by the Australian Government Actuary demonstrates that incorporating a longevity component into retirement income solutions can boost income by 15–30% compared with drawing the minimum amount from an account-based pension, whilst delivering more stable income over time.

Lifetime income products provide a reliable income stream for life, managing longevity risk whilst allowing account-based pension components to be drawn at higher, more efficient rates. For means-tested retirees, the favourable Age Pension treatment of lifetime income products creates additional financial benefits.

From Why to How

At Optimum Pensions, we strongly support these best practice principles. They represent a maturation of thinking about retirement income—moving beyond products in isolation towards integrated solutions that genuinely serve members’ needs.

The question for trustees is no longer why to include lifetime income components in retirement solutions, but how.

This is where practical implementation becomes crucial. Trustees face complex requirements under a plethora of legislation and regulations. Designing and running a lifetime income stream product introduces operational risks and long-term obligations that endure for members’ lifetimes.

Our Implementation Guide

To support trustees navigating this landscape, Optimum Pensions has developed a comprehensive Implementation Guide for Principle 9. Our guide addresses the practical questions trustees are asking:

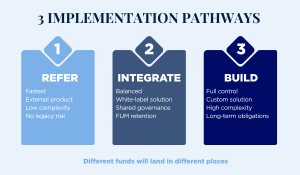

- What are the different pathways to implementation: refer, integrate or build?

- How do funds balance control, speed to market and legacy risk?

- Where can funds leverage existing infrastructure rather than building from scratch?

- What questions will boards ask, and how should they be answered?

We’ve distilled these insights into a Fast Track Guide available now, with the full comprehensive guide to follow.

The best practice principles represent an opportunity to genuinely improve retirement outcomes for millions of Australians.

Download our Fast Track Implementation Guide today.