Principle 9: Why Trustees Should Act Now on Retirement Income

Australia’s superannuation industry stands at a defining moment. Treasury’s proposed Best Practice Principles for retirement income solutions have shifted the conversation from whether funds should offer lifetime income products to how they should implement them effectively.

The principles are still in consultation, not yet finalised. But forward-thinking trustees aren’t waiting—and here’s why you shouldn’t either.

The Direction Is Clear

Treasury’s consultation paper leaves no ambiguity about regulatory expectations. The proposed Principle 9 calls for trustees to construct at least one retirement income solution that includes a lifetime income product component, designed with regard to likely Age Pension eligibility and integrated with account-based pension drawdown strategies.

This is a clear signal of where the Retirement Income Covenant is heading. The government has flagged what it expects trustees to deliver. Waiting for final principles means falling behind funds already building capability, testing solutions, and positioning themselves as retirement income leaders.

But This Isn’t Just About Compliance

Even without finalised principles, the case for lifetime income solutions stands on its own merit: better outcomes for members.

Research by the Australian Government Actuary demonstrates that incorporating a longevity component can boost retirement income by 15–30% compared with minimum drawdowns from an account-based pension alone, whilst delivering greater income stability throughout retirement.

For means-tested retirees, which are many of your members, the benefits multiply. The favourable Age Pension treatment of lifetime income products creates additional financial advantages that can materially improve retirement living standards.

Treasury’s discussion paper emphasises that one product alone cannot balance the three objectives of the Retirement Income Covenant. Members need solutions that simultaneously maximise income, manage longevity and inflation risks, and maintain flexible access to capital. Including lifetime income products into your product suite allows you to offer better solutions so your members can achieve this balance.

The Challenge: Where Do We Start?

This is where many trustees get stuck. The intent is clear, the member benefits are compelling—but the path forward feels complex.

Trustees face intricate requirements across multiple regulatory frameworks: SPS 515’s strategic planning obligations, CPS 230’s operational risk standards, the Best Financial Interests Duty, DDO requirements, and evolving advice frameworks under DBFO reforms. Designing and running a lifetime income product introduces operational risks and long-term obligations that endure for members’ lifetimes.

How do you balance speed to market against legacy risk? Where can you leverage existing infrastructure rather than building from scratch? What questions will your board ask, and how should you answer them?

Your Implementation Roadmap

We’ve developed a comprehensive Principle 9 Implementation Guide specifically to answer these questions.

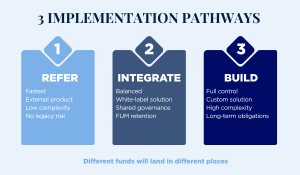

The guide maps three distinct pathways:

Refer to an external provider—fastest to market, lowest complexity, no legacy risk, but less control and member integration.

Integrate a white-label solution—balanced approach enabling fund-branded experience with streamlined governance, potential FUM retention, and shared infrastructure.

Build in-house—maximum control and customisation, but higher complexity, longer timelines, significant regulatory lift, and permanent legacy obligations. We discuss customisation options in detail, including the “Accumulation IRIS”, which, like other IRIS product types, can be achieved either with an insurer or stand alone under a Group Self Annuitisation arrangement.

Each pathway involves three critical integration layers:

Each pathway involves three critical integration layers:

Member Experience (calculators, communications, advice pathways),

Product & Rules (design, pricing, compliance frameworks), and

Administration & Plumbing (systems, data, operations, longevity risk management).

Our guide provides:

- Detailed analysis of trade-offs across all three pathways

- The board questions you’ll face and how to answer them

- Regulatory frameworks affecting each approach

- The Solution Stack—breaking down what you need at each layer

- A Principle 9 Readiness Checklist to assess your starting position

- Practical next steps for moving from decision to implementation

The Time to Move Is Now

Fourteen funds and providers are already in the market. There’s no first-mover advantage—but there is mounting risk in being a late follower as member expectations rise and regulatory scrutiny intensifies.

You don’t need to wait for finalised principles to start building capability. The direction is set. The member benefits are proven. The question is simply which pathway fits your fund’s strategy, resources, and member needs.

Download our comprehensive Principle 9 Implementation Guide

Then reach out to discuss your pathway forward.