Embrace Equity: International Women’s Day 2023

International Women’s Day is an excellent time to reflect on the gender gap in superannuation savings and retirement outcomes.

On average Australian Women:

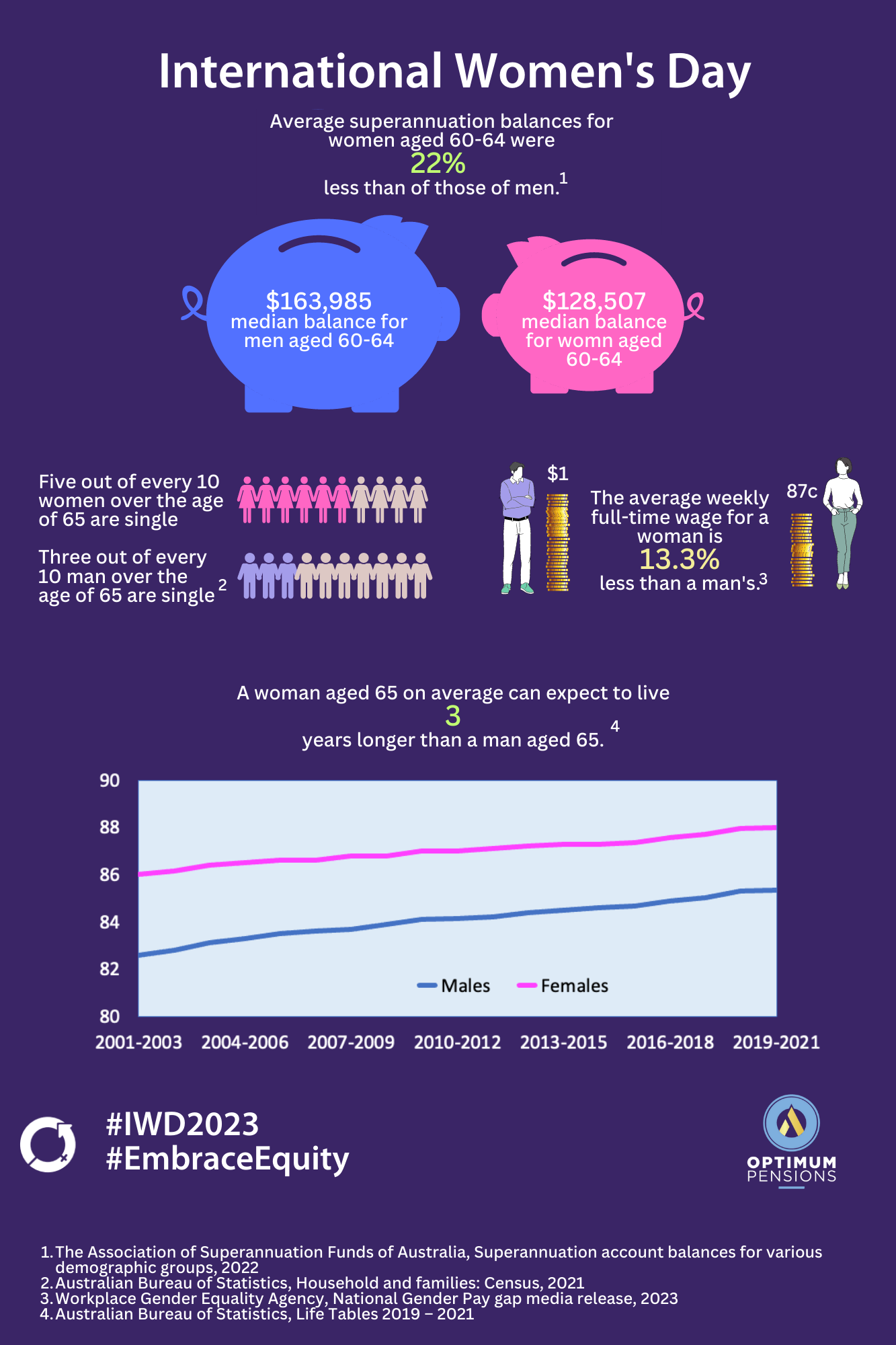

- retire with 23% less super than men[1]

- are more likely to have broken work patterns

- earn 13.3% less than men[2]

- live longer than men[3]

- aged 55 and over is the fastest growing cohort of homeless Australians[4]

The data shows that the gender gap is closing, but Women’s average account balances are still substantially lower than Men’s at all ages. It is also a concern that around 23 per cent of females in the 60 to 64 age group have no superannuation compared to 13 per cent of males.

Debby Blakey, CEO of HESTA, calls the super gender gap the “motherhood penalty”, where women have less in their super because they take time out of the workforce to care for children.

Debby Blakey, CEO of HESTA, calls the super gender gap the “motherhood penalty”, where women have less in their super because they take time out of the workforce to care for children.

Equality versus Equity: What’s the difference?

The theme of International Women’s Day this year is #EmbraceEquity and that is a great message for our superannuation industry. The theme aims to get the world talking about why “equal opportunities are no longer enough”.

So, what’s the difference between equity and equality and why is it important to understand, acknowledge and value this? And in the superannuation industry specifically – how can this understanding help us consider the gender differences in retirement outcomes?

#EmbraceEquity refers to the fact that treating everyone equally can actually exclude and limit people. Equity recognises that each person has different circumstances and needs different things to reach an equal outcome.

The image below illustrates equality when each individual (or group of people) is given the same resources or opportunities, whereas equity recognises that each person has different circumstances and allocates the exact resources and opportunities needed to reach an equal outcome.

This is nicely summed up by Susan K Gardner. Dean, College of Education, Oregon State University, “Equality is giving everyone a shoe. Equity is giving everyone a shoe that fits.”

Equity is a long-term and sustainable solution and is a process for addressing imbalanced social systems. Equity-based solutions consider the diverse lived experiences of individuals and communities, adapting services and policies according to these differences. That is how we need to consider the gender difference in retirement outcomes.

Equality is giving everyone a shoe. Equity is giving everyone a shoe that fits.”

Susan K Gardner. Dean, College of Education, Oregon State University

Improving Women’s retirement outcomes

International Women’s Day aims to create a gender equal world. This means closing the gap in women’s financial inequality, including superannuation and retirement.

There is a simple way to improve the retirement outlook for Australian Women: address the gender pay gap. But that is not a quick fix, so we need a range of targeted measures to improve Women’s superannuation balances.

A great example of such an initiative was the abolition of the $450 a-month wages threshold for payment of compulsory superannuation, which came into effect on 1 July 2022. Around two-thirds of those affected by the threshold are female.

Several superannuation funds and industry bodies are calling for the payment of superannuation on the Commonwealth Paid Parental Leave (PPL) scheme. Almost all recipients of PPL are Women.

In addition to superannuation on paid parental leave, Women in Super propose introducing a “carer credit” to compensate parents for superannuation lost due to unpaid parental leave. ASFA has a similar proposal called a baby bonus paid directly into the person’s superannuation account when they take a break from the workforce to have children.

A factor that is often not talked about when discussing the gender gap in retirement outcomes is financial literacy. However, research by Alison Preston and Robert E. Wright found that a gender gap in financial literacy may account for about 8.5% of the gap in superannuation savings between male and female Australians[5].

Women’s financial literacy is a real concern. It should be a concern for all of society.”

Professor Alison Preston

Let’s #EmbraceEquity – together!

To embrace something is to willingly and enthusiastically accept, adopt, and espouse it. Optimum Pensions encourages the Government and the Industry to embrace equity and improve women’s financial security in retirement.

Furthermore, we encourage Women to invest in themselves and their own future financial security. To be proactive, investigate and secure retirement solutions that will suit their needs and boost their confidence in retirement.

—

[1] The Association of Superannuation Funds of Australia, Superannuation account balances for various demographic groups, 2022 [2] Workplace Gender Equality Agency, National Gender Pay gap media release, 2023 [3] Australian Bureau of Statistics, Life Tables 2019 – 2021, 2022 [4] Australian Human Rights Commission, Older Women’s Risk of Homelessness: Background Paper 2019 [5] Preston, Alison and Wright, , Robert E., Gender, Financial Literacy and Pension Savings, 2022[/vc_column_text][vc_column_text] ***

Optimum Pensions was launched in 2017 with a single mission – to help Australians lead a comfortable retirement. The Optimum Pensions innovative retirement income solutions are specifically developed to address longevity risk and provide greater peace of mind for all retirees; no matter how long they live.

The Optimum Pensions, award-winning LifeSpan Calculator builds confidence around personal life expectancy and retirees’ possible retirement planning horizon.