The Housing Wealth Divide Redefining Retirement Security

In our previous article, we explored the confidence crisis facing Australian retirees and identified planning as the game-changing intervention. Yet even the most meticulous planning can be undermined by structural shifts in the retirement landscape. This article examines the housing crisis that’s creating a new retirement divide—one that challenges fundamental assumptions about retirement income adequacy.

When Assumptions Break Down

The Australian retirement income system has long operated on an implicit assumption that retirees will own their homes outright. This assumption underpins everything from Age Pension adequacy calculations to superannuation withdrawal strategies and retirement income benchmarks. It’s breaking down rapidly, with profound implications for retirement security.

More than one in three Millennials now expect to carry mortgage debt into retirement, along with one in four Baby Boomers. This stands in stark contrast to current retirees, only 8 per cent of whom are still paying off a mortgage. The impact on confidence is severe—48 per cent of retirees with a mortgage report low confidence, compared to 28 per cent of all retirees.

Simultaneously, the proportion of retirees renting privately has doubled from 6 per cent to 12 per cent between 2003 and 2023, while outright homeownership has fallen from 75 per cent to 66 per cent. This trend shows no sign of reversing. Declining homeownership rates among younger cohorts suggest the proportion of retirees who rent will continue to grow substantially over the coming decades.

The Stark Reality for Renters

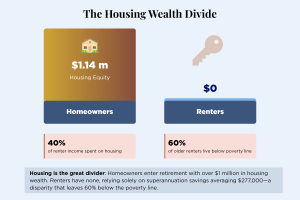

Renters face acute financial pressure in retirement. They spend approximately 40 per cent of their total household expenditure on housing—a burden that fundamentally undermines retirement security. Nearly 60 per cent of older renters live below the poverty line, a stark indicator of systemic failure.

While the Age Pension provides adequate support for homeowners, it leaves the typical single renter 23 per cent below the poverty line even with Commonwealth Rent Assistance. This gap between policy design and lived reality creates a growing crisis that superannuation alone cannot solve.

The wealth divide created by housing status is stark and growing.

The average homeowner possesses housing equity exceeding $1.14 million, while the average renter holds superannuation savings of just $277,000—and no housing wealth at all. This disparity represents one of the most significant fault lines in retirement security and challenges fundamental assumptions about retirement income adequacy.

The Expectations Gap

The housing crisis intersects with another significant shift: changing retirement timing and income expectations. The median retirement age has increased by five years for both genders since 2003, with women now retiring at 64 and men at 65. The proportion of women retiring before age 55 has collapsed from 26.4 per cent to just 7.3 per cent, while those retiring between 65 and 69 has nearly tripled from 11.7 per cent to 31.6 per cent.

Yet retirement timing is only part of the story. Income expectations reveal another significant disconnect. Australians under 45 estimate they will need household income of $100,000 per year in retirement. Those aged 25 to 34 expect even more—$106,000 annually, representing a 59 per cent increase in expectations since 2023.

The reality is quite different. Current retiree couples report actually spending an average of $55,000 per year, while the ASFA Comfortable Lifestyle benchmark sits at $73,077 for couples who own their home outright. Note the critical assumption embedded in that benchmark: homeownership. For the growing number of Australians who will rent in retirement, these figures bear little relationship to their actual needs.

What This Means for Funds

Traditional retirement income strategies assume housing security. They will not serve the growing proportion of members who will be renting or carrying mortgage debt into retirement. Superannuation funds need distinct approaches and income adequacy benchmarks that reflect these diverse housing circumstances.

The expectation gap is not merely academic—it drives anxiety and fundamentally shapes retirement planning behaviour among younger Australians. Members need realistic income education delivered well before retirement, helping them understand what a comfortable retirement actually costs in their specific circumstances and how their superannuation can support it.

For members who will rent in retirement, the conversation must be fundamentally different. Their superannuation will need to deliver higher ongoing income to cover housing costs, which means different drawdown strategies, different product mixes, and potentially different accumulation strategies decades before retirement.

The Retirement Income Covenant requires funds to formulate strategies that assist members in achieving and balancing retirement income objectives. When fundamental assumptions about housing no longer hold, those strategies must evolve. Funds that continue to plan as if all members will be homeowners will fail a growing proportion of their membership.

Next in This Series

Part 3: The Gender Retirement Gap: The confidence crisis and housing divide don’t affect all Australians equally. Women face systemic disadvantages across every dimension of retirement readiness. Only 41% of women feel confident about retirement compared to 59% of men. Single mothers in their 40s—just 19% confident—represent the most vulnerable group measured. Life events between ages 45 and 65 function as financial shocks that disproportionately derail women’s retirement preparation. What must funds do to address these deeply entrenched inequalities?

Sources

HILDA Survey Statistical Report 2025

Vanguard, How Australia Retires 2025