Superannuation – The Unfinished System

Why the Retirement Phase Still Lags, and What Trustees Must Do Next

On 1 July 1992, the Superannuation Guarantee came into force and changed the financial trajectory of a nation. What Paul Keating set in motion that day was, by any measure, one of the great feats of social policy in Australian history. Over three decades later, Australia manages the fourth-largest pool of pension assets in the world. By the accumulation measure, the only one we have consistently applied, the system has been a success.

But accumulation was always only half the job.

When a member retires, the financial logic of superannuation reverses entirely. For decades, the system collected, invested and grew. At retirement, it needs to distribute reliably, sustainably, and for as long as the member lives. That is a fundamentally different task. And for most of the system’s history, it has effectively been deferred.

The diagnosis has been consistent

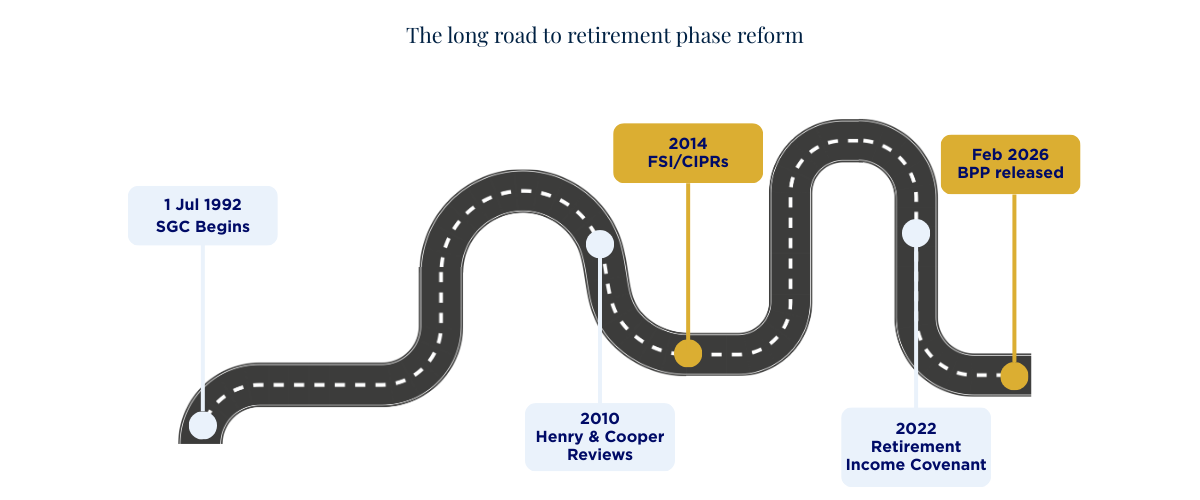

The retirement income gap was called out clearly in the 2010 Henry Review Report, which identified a lack of suitable retirement income products and noted that few Australians were managing longevity risk through lifetime income products. That was sixteen years ago.

The diagnosis has since been repeated with remarkable consistency. Jeremy Cooper, who chaired the 2010 Super System Review, put it plainly in 2017: “Reliable retirement income should be the core business of super funds. Too many are acting like it isn’t.” He observed that the vast majority of members would either face the risk of running out of money during retirement or live with a lower standard of living through fear of doing so. That was not a fringe view. It reflected the emerging consensus of a decade of inquiry.

“Reliable retirement income should be the core business of super funds. Too many are acting like it isn’t.”

— Jeremy Cooper, Chairman of Retirement Income at Challenger, 2017

The list of reviews, frameworks and policy interventions since Henry is substantial: the 2010 Cooper Review; the 2014 Financial System Inquiry (FSI), which proposed Comprehensive Income Products for Retirement (CIPR) and seriously canvassed making lifetime income product offerings mandatory; the 2018 Australian Government Actuary report on retirement income products; the Retirement Income Covenant, announced in the 2018-19 Budget and legislated in 2022; a 2023 Treasury discussion paper on the retirement phase; and now, in February 2026, Treasury’s Best Practice Principles for Superannuation Retirement Income Solutions (BPP), released alongside a new Retirement Reporting Framework.

Each was a genuine contribution. Each also acknowledged, implicitly or explicitly, that the previous steps had not been sufficient.

Progress, and its limits

It would be unfair, and inaccurate, to say nothing has changed. The policy environment has shifted materially. Regulators are asking harder questions. Most large funds now have people with “retirement” in their title, some at senior levels. A growing number have launched lifetime income products or meaningfully improved their account-based pension offerings. Retirement planning tools that did not exist five years ago are now increasingly standard.

To their credit, many funds have moved well beyond the point of handing a member a cheque and wishing them well. The farewell handshake has given way, in many cases, to genuine retirement support frameworks, better member communications, and more sophisticated drawdown strategies. That shift deserves acknowledgement. The question is whether the pace matches the need.

The BPP themselves are substantive. They ask trustees to segment their membership into meaningful cohorts, design fit-for-purpose solutions for those cohorts and, critically, provide access to a lifetime income product beyond the Age Pension. The accompanying Retirement Reporting Framework will have APRA collecting and publishing data on fund offerings and member outcomes, a transparency mechanism that has been conspicuously absent from the retirement phase until now.

The thread running from the FSI’s proposed CIPRs through to the BPP is worth acknowledging: the policy system has been working, in its deliberate way, towards the same destination. Where the FSI contemplated making lifetime income product offerings mandatory, the BPP makes it best practice. Voluntary, yes, but clearly signalled as the direction of travel.

The gap between articulation and action

We are now over fifteen years on from the Henry Review Report. The Retirement Income Covenant has been in force for nearly four years. Subsequent regulator reviews have found implementation to be slower than the urgency warrants. And when Optimum Pensions surveyed industry leaders on the 30th anniversary of compulsory superannuation in 2022, the consistent answer to “what still needs to be done?” pointed squarely at the retirement phase.

Meanwhile, the cohort arriving at retirement with meaningful superannuation balances, the first generation for whom the system operated across most of their working lives, is not waiting for the policy architecture to finalise. Around 800,000 Australians intend to retire in the next five years. More than 2.5 million Australians are expected to retire in the next decade. Many will have accumulated balances that deserve better than a default account-based pension and a good luck wish.

The problem is not that the system is broken. It is that we have become highly capable at describing the problem—producing thoughtful reviews, frameworks and principles—while the pace of change in actual member outcomes trails behind. At some point, a fund must decide what products it will offer…and then actually offer them.

There is also a structural temptation to hold out for a complete solution. The retirement phase is genuinely complex with longevity risk, sequencing risk, inflation, cognitive decline, Age Pension interactions and the diversity of member circumstances. No single product or pathway resolves all of this. But complexity is not an argument for inaction. The absence of a perfect solution has never been a reason to avoid a good one.

What the BPP asks of trustees

The BPP are the most specific and actionable guidance the retirement phase has yet received: cohort-based design, fit-for-purpose product suites, access to lifetime income, genuine member engagement, and regular review.

Underlying all of it is a clear, if understated, model of what members actually need. First, access to a portfolio of suitable products, including, critically, lifetime income options that the BPP explicitly identifies as best practice to offer. Second, a decision support architecture that helps members find their way to the right solution given their circumstances, their level of engagement and their risk appetite. Not every member will want to make active choices. Not every member can. Good retirement outcomes require both the right products and the right guidance to reach them. The BPP points at both.

The accompanying Retirement Reporting Framework adds meaningful accountability. When APRA publishes data on what funds are actually offering and what outcomes members are actually experiencing, the gap between those who have acted and those who have not will become visible to everyone: trustees, regulators and members alike.

The principles are voluntary. Acting on them is a choice. But it is increasingly difficult to argue that the choice should wait.

The obligation that remains

Three decades is a long time to be completing the first half of a job. The accumulation system Paul Keating launched in 1992 has given millions of Australians financial resources they would not otherwise have had. They deserve a retirement phase equal to that ambition.

The obligation is perhaps best captured by a teaching from Pirkei Avot, attributed to Rabbi Tarfon, that has resonated across centuries precisely because large, necessary work rarely has a clean finishing line:

“It is not your duty to finish the work, but neither are you at liberty to neglect it.”

— Rabbi Tarfon, Pirkei Avot 2:16

The work of building a superannuation system that genuinely serves members from first contribution to last payment remains unfinished. That is not a condemnation. The task is large, the complexity is real, and the progress, however uneven, is genuine. But the obligation to continue does not diminish because the work is difficult.

The Best Practice Principles are an invitation to act. The members retiring in the next five years are reason enough to accept it.

##