Why Half of Australians Don’t Feel Confident About Retirement

Approximately 2.5 million Australians are projected to move into the retirement phase within the next 10 years, with recent figures showing 710,000 people intend to retire in the next five years, including 226,000 within the next two years.

For policymakers and superannuation fund trustees, the more we understand about these Australians, the better we can help them prepare for this critical life transition. This is especially relevant for the trustees as they review their retirement income strategies.

Four major research reports released in recent months—the HILDA Survey, Vanguard’s How Australia Retires, AMP’s Retirement Confidence Pulse, and Impact Economics’ analysis for the SMC of women’s economic security—provide unprecedented insight into this cohort. Collectively, these studies surveyed more than 5,800 Australians and analysed 23 years of longitudinal data. Their convergent findings reveal fundamental shifts in the retirement landscape that demand attention from superannuation funds.

This is the first in a three-part series exploring what we now know about Australians approaching retirement. This article examines the confidence crisis and identifies planning as the game-changing intervention. The second article will explore the housing wealth divide that’s redefining retirement security. The third will examine why women face disproportionate challenges and what funds must do to address systemic inequalities.

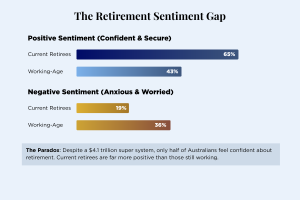

The Confidence Paradox

Australia has the world’s fifth-largest pension market, with a superannuation system now valued at $4.1 trillion and projected to reach $10 trillion by 2040. Yet despite this unprecedented accumulation of wealth, only half of Australians feel financially confident about their retirement, according to the AMP Retirement Confidence Pulse. AMP Chief Executive Alexis George describes the finding as a “national wake up call,” noting that “despite national wealth, a maturing super system and growing balances, too many don’t have financial peace of mind about their retirement.”

The research reveals a striking sentiment gap between current retirees and those approaching retirement. Sixty-five per cent of current retirees report positive sentiment, describing themselves as confident and secure. In contrast, only 43 per cent of working-age Australians share this positive outlook. The inverse is equally concerning: 36 per cent of working-age Australians report negative sentiment—feeling anxious or worried about retirement—compared to just 19 per cent of retirees.

This paradox suggests a fundamental disconnect between superannuation system outcomes and member perceptions. The wealth exists, but the confidence doesn’t. For funds, this represents both a challenge and a significant opportunity to improve member outcomes through better guidance, communication, and support.

Planning is the Game-Changer

The research identifies retirement planning as the single most influential factor in determining confidence, yet nearly half of working-age Australians have no plan for how they will retire. Among those aged 55 to 64 who are still working—the cohort closest to retirement—only 29 per cent describe themselves as well-planned. Perhaps most concerning, 38 per cent of current retirees report they had no plan when they retired.

The impact of planning is dramatic and quantifiable. Vanguard’s research presents the case of “Sam,” a typical 38-year-old Australian with a baseline 41 per cent probability of positive retirement sentiment and 49 per cent probability of negative sentiment. When Sam undertakes five key actions—with having a retirement plan being the most influential—the outlook transforms completely. Positive sentiment probability more than doubles to 89 per cent, while negative sentiment plummets to just 8 per cent.

The planning effect is perhaps most clearly illustrated in retirement timing expectations. Working-age Australians with no plan face a gap of 9.7 years between their ideal retirement age and when they realistically expect to retire. For those with a detailed plan, this gap shrinks to just 0.3 years. Among current retirees, those who had a clear plan were three times more likely to feel highly confident about funding their lifestyle and 65 per cent more likely to maintain a positive outlook overall.

This evidence creates a clear imperative for funds under the Retirement Income Covenant. Planning support is demonstrably the highest-impact intervention funds can make, and members want it—86 per cent of working-age Australians believe it’s important for their fund to provide guidance up to and through retirement.

The Path Forward

The confidence crisis is real, but it’s also solvable. The evidence is clear that planning transforms retirement outcomes. Members who engage in retirement planning are more likely to retire when they want to, feel confident about their financial security, and maintain positive sentiment throughout retirement. Those without a plan face nearly a decade of unwanted work, pervasive anxiety, and uncertainty about their future.

For superannuation funds, this represents both an obligation and an opportunity. The Retirement Income Covenant requires funds to assist members approaching retirement. The research shows exactly how to deliver the highest-impact support: accessible, engaging retirement planning tools and guidance that help members create and maintain clear plans.

Yet planning alone cannot solve all the challenges facing Australian retirees. Even the most meticulous planning can be undermined by structural shifts that are redefining what retirement looks like—and what it costs.

Next in This Series

Part 2: The Housing Wealth Divide: The Australian retirement system assumes members will own their homes outright. That assumption is breaking down rapidly. One in three Millennials expect to carry mortgage debt into retirement, while the proportion of retirees renting has doubled. The wealth gap this creates is stark: homeowners enter retirement with over $1 million in housing equity, while renters have none. How should funds respond when fundamental planning assumptions no longer hold?

Sources

HILDA Survey Statistical Report 2025

Vanguard, How Australia Retires 2025