The Gender Retirement Gap: Why Women Face Disproportionate Challenges

This series has examined the confidence crisis facing Australian retirees and the housing wealth divide that’s redefining retirement security. This final article explores how these challenges—and others—affect women disproportionately, creating systemic inequalities that demand gender-aware strategies from superannuation funds.

A Persistent Gap Across All Dimensions

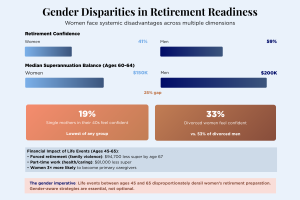

Gender disparities permeate retirement outcomes. Only 41 per cent of women feel confident about retirement compared to 59 per cent of men. This confidence gap is underpinned by persistent superannuation disparities—women aged 60 to 64 hold median balances 25 per cent lower than men, with the gap peaking at 32 per cent for those aged 50 to 54. Women receive on average $1,081 less in employer contributions each year.

Women aged 60 to 64 hold median superannuation balances 25 per cent lower than men. The gap peaks earlier, reaching 32 per cent for those aged 50 to 54—the critical pre-retirement accumulation years. This disparity stems from multiple sources: women receive on average $1,081 less in employer contributions each year, reflecting lower lifetime earnings, more time spent in unpaid care work, and the persistent gender pay gap.

But the superannuation gap tells only part of the story. The research reveals that life events between ages 45 and 65—a critical window for final retirement preparation—function as financial shocks that disproportionately set women back.

Life Events as Financial Derailment

Women are three times more likely than men to become primary caregivers between ages 45 and 65. This responsibility, whether caring for ageing parents, sick partners, or family members with disabilities, dramatically reduces their ability to participate in paid work. The reduction in earnings can be as large as $40,000 per year, with corresponding impacts on superannuation accumulation precisely when they should be building final retirement savings.

The financial impact of other life events is equally stark. A woman forced to stop working at age 50 due to family violence can expect to have $94,700 less in superannuation by age 67. Reducing to part-time work from age 50 due to health or caring responsibilities can cost $81,000 in retirement savings. These are not hypothetical scenarios—they represent the lived experience of hundreds of thousands of Australian women.

Divorce at age 50 leaves separated women aged 60 to 69 with median superannuation balances 38 per cent lower than their partnered peers. While men’s economic security is often relatively unaffected by separation, women face heightened risk of poverty, particularly if they do not re-partner. Over a quarter of women have experienced violence from a partner or family member, with financial abuse affecting 16 per cent of women and creating lasting economic harm that extends well into retirement.

Acute Vulnerability

The vulnerability is most acute for specific groups. Single mothers in their 40s register just 19 per cent confidence, the lowest of any demographic measured across all the research. These women face the perfect storm: lower superannuation balances, ongoing dependent care responsibilities, reduced workforce participation, and limited time to recover financially before retirement.

Divorced women report 33 per cent confidence compared to 53 per cent of divorced men, a 20 percentage point gap that reflects fundamentally different economic outcomes from the same life event. Single women over 50 are 25 per cent more likely to face poverty than partnered women, and this vulnerability only intensifies in retirement.

What Gender-Aware Strategies Look Like

These disparities demand that superannuation fund trustees recognise the critical importance of the 45 to 65 age window for women and provide targeted support during this period. Gender-aware strategies must account for the financial impact of caregiving, health challenges, family violence, and divorce—not as edge cases, but as common experiences that shape women’s retirement trajectories.

This means different communication approaches that acknowledge women’s lived experiences. It means retirement planning tools that account for interrupted careers and part-time work. It means understanding that a woman’s superannuation balance at age 50 may tell a very different story than a man’s—and that the final 15 years before retirement may look fundamentally different.

It also means recognising intersectionality. Single mothers, divorced women, renters, and those who’ve experienced violence face compounding disadvantages. Strategies that treat all members identically will systematically fail those who need support most.

Looking Ahead: Four Imperatives for Funds

This series has examined the evidence from four major research reports released in 2025. Together, they paint a clear picture of Australian retirement readiness—and the work that remains. Four imperatives emerge for superannuation fund trustees as they review their Retirement Income Strategies.

First, close the planning gap. Planning is demonstrably the highest-impact intervention available. Nearly half of working-age Australians have no retirement plan, yet those with detailed plans can retire when they want to, feel confident about their security, and maintain positive sentiment throughout retirement. Funds must make accessible, engaging retirement planning support a priority and not an afterthought.

Second, abandon outdated housing assumptions. Traditional retirement income strategies assume members will own their homes outright. One in three Millennials expect mortgage debt in retirement. The proportion of retirees renting has doubled and continues to rise. Funds need distinct approaches and income adequacy benchmarks for members who will rent or carry debt—not one-size-fits-all strategies that systematically fail growing cohorts.

Third, address the expectations gap. Young Australians expect to need nearly double what current retirees spend. This gap drives anxiety and shapes planning behaviour, yet much of it stems from misunderstanding rather than genuine need. Members need realistic income education delivered well before retirement, helping them understand what a comfortable retirement actually costs and how their circumstances (especially housing status) affect these calculations.

Fourth, implement gender-aware strategies. Life events between ages 45 and 65 disproportionately derail women’s retirement preparation. Single mothers, divorced women, and survivors of violence face acute vulnerability. Approaches that treat all members identically will systematically fail those who need support most. Gender-aware strategies are not optional—they’re essential for equitable outcomes.

The challenge facing the Australian superannuation system is not primarily one of accumulation—the $4.1 trillion system demonstrates wealth-building success. The challenge is confidence, capability, and support. Members are anxious despite unprecedented savings. They lack plans despite clear pathways. They face structural inequalities despite regulatory protections.

Funds that respond to these evidence-based insights with innovative strategies and member-centric guidance will deliver materially better outcomes. The data is clear. The pathways are evident. The question now is: how will funds respond?

Sources

HILDA Survey Statistical Report 2025

Vanguard, How Australia Retires 2025