Balancing retirement income and access to capital: A financial planning case study

A retirement income strategy is no longer a binary choice between a guaranteed annuity and an investment account.

Approaching retirement, many Australians will be engaging financial planners to help them solve the retirement trilemma: maximising retirement income, having flexible access to funds and managing the associated risks.

Since the SIS legislation was changed so that superannuation funds and insurers could offer new innovative income products, such as investment-linked annuities (ILAs), we have seen an expansion in the range of options retirees have available to meet their needs. Financial planners can now combine different product types to help their clients solve the retirement trilemma.

This case study illustrates how product combinations can deliver superior outcomes that are more in line with each retiree’s unique risk preferences, retirement goals and circumstances. Financial planners can help their clients with hybrid strategies that maximise sustainable income streams while allowing flexibility, giving their clients the best of both worlds.

Vanessa and Simon visit their financial planner.

Vanessa and Simon are both 67 and about to retire. They visit Marie, their financial planner, for advice.

Vanessa and Simon are married with two adult children. They own their own home, which is worth about $2 million. Vanessa has $450,000 in super, and Simon has about $700,000. They have private savings of about $75,000 and other personal assets of $25,000. They don’t intend to leave any specific inheritance to their children.

Their main goals are to enjoy an active retirement lifestyle early on, with travel, and to be confident they’ll always have sufficient income without running out of money as they age, even if one spouse outlives the other.

Marie starts by helping Vanessa and Simon consider how confident they want to be that their retirement plan will last as long as at least one of them is still alive. She uses the Optimum Pensions Lifespan Calculator to explore different confidence levels. Vanessa and Simon opt for the highest confidence level, 90%. This confidence level means there is a high probability that the retirement planning horizon they use will cover the lifespans of people like them.

Considering their personal health and lifestyle characteristics, the Lifespan Calculator calculates that for Vanessa and Simon to be 90% confident that their plan will cover them as long as either person lives, they should have a retirement plan that lasts for 36 years, up to age 103.

Vanessa and Simon comment that this is much higher than average life expectancy. Marie explains that life expectancy figures are based on averages, and half of the people will live longer than their life expectancy. To be 90% confident, their planning horizon has to be long enough to cover 90% of people like them, not 50%.

Marie then suggested the following three scenarios using different combinations of retirement income products to meet the couple’s needs:

- Investing all of their $1,150,000 superannuation in a balanced option of an Account Based Pension (ABP);

- Investing all their $1,150,000 superannuation in a balanced option of an ILA; and

- Investing their $1,150,000 superannuation in a combination of a balanced option of an ABP and a balanced option of an ILA product.

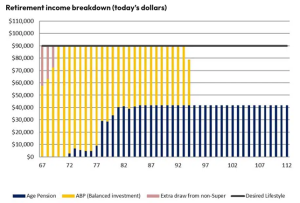

Scenario 1: Vanessa and Simon invest 100% of their superannuation in ABPs

Marie generates a projection of Vanessa and Simon’s retirement income. In this scenario, she assumes Vanessa and Simon make withdrawals from superannuation to meet a total spending level of $90,000 per year (linked to price inflation). The projection shows they could spend $90,000 annually until age 93, reducing to just under $80,000 at age 94. The ABPs would then run out, and Vanessa and Simon would only have the Age Pension to live on thereafter, short of the target planning age of 103.

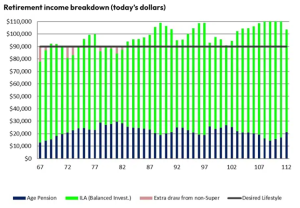

Scenario 2: Vanessa and Simon invest 100% of their super into an ILA

Vanessa generates an illustration of what this could look like if they invest fully in an ILA. The illustration above shows that their goal of $90,000 per year could be met until age 103 and beyond, with the ILA providing longevity protection. However, this approach gives them little to no access to additional capital other than their separate savings for emergencies or one-off expenses.

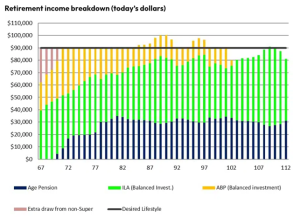

Scenario 3: Vanessa and Simon invest $700,000 into an ILA and $450,000 into an ABP

This combination approach allows Vanessa and Simon to enjoy their desired $90,000 goal until age 101, with a slight reduction to around $80,000 after that age. Importantly, this combination provides longevity protection through the ILA portion while allowing flexible access to capital via the ABP.

The benefits of an integrated retirement income solution

The analysis shows Scenario 3, combining an ILA and ABP, provides the best outcome for Vanessa and Simon by maximising their income goals, managing longevity risk, and allowing access to capital. Specifically, the combined approach delivers:

- Sustainable lifetime income: The ILA component ensures Vanessa and Simon receive income that’s guaranteed to continue for life, even if one spouse outlives the other significantly.

- Access to capital: The ABP allows flexible withdrawals to meet discretionary spending goals, such as travelling early in retirement and managing unexpected expenses.

- Earlier Age Pension Access: The ILA’s concessional Age Pension treatment enables earlier access to government support from the Age Pension.

- Potential legacy: Any remaining ABP capital on death can provide a bequest to their children upon the second spouse’s passing.

The case study highlights how traditional ABPs alone may allow full access to capital but fail to adequately manage longevity risk. It exemplifies the versatility of using newer products like ILAs, which can provide income that is guaranteed to continue for life. Most importantly, it demonstrates the benefits of an integrated retirement income solution tailored to each retiree’s unique needs and goals by blending different product characteristics.

As a professional financial planner, Marie has added significant value by guiding her clients through complex retirement decisions, assessing trade-offs, and constructing synchronised product strategies to maximise their outcomes. The case study reinforces the evolving role of financial advice in securing holistic, sustainable retirement income solutions that clients and planners can be confident in.

This case study is just one of several in our book “Retirement Income for Life: A Guide for Financial Planners”.

The book is an essential guide for financial planners dedicated to helping clients build a secure retirement income strategy. It expertly addresses the challenges of rising life expectancy, providing strategic insights to ensure a confident and fulfilling retirement. Balancing client retirement lifestyle expectations with the range of retirement income options available in the Australian market, the guide takes a practical approach, offering actionable steps to implement key principles. Real-world case studies bring these concepts to life, showcasing successful strategies that financial planners can readily apply.

Assumptions used in this case study

- Rather than using a fixed rate of return (i.e., the same return every year), Marie used historical investment performance since 1998 to illustrate an example of their potential variable income each year. The calculations are presented in today’s dollars, allowing for historic inflation rates over that period.

- Marie assumes that the ABP has administration and investment fees of 0.6% a year.

- The assumed fees on the ILA product are 1.2% a year – made up of 0.9% in administration and longevity insurance fees and 0.3% per annum for investment fees.

- The rate of income from the ILA is based on pricing from Generation Life’s LifeIncome product, using the 2.5% LifeBooster option, a 65% reversionary pension if Simon dies before Vanessa, and a 50% reversionary pension if Vanessa dies before Simon.

- The Age Pension income level and the means-testing threshold levels are assumed to increase in line with (historic) price inflation.

Authors: David Orford, Jim Hennington & Peter Rowe[/vc_column_text][vc_column_text]***

Optimum Pensions was launched in 2017 with a single mission – to help Australians lead a comfortable retirement. The Optimum Pensions innovative retirement income solutions are specifically developed to address longevity risk and provide greater peace of mind for all retirees; no matter how long they live.

The Optimum Pensions, award-winning LifeSpan Calculator builds confidence around personal life expectancy and retirees’ possible retirement planning horizon.