How Long Do Australians Really Live – and Why It Matters for Member Outcomes

For many Australians approaching retirement, the question isn’t just “how much do I have?” but “how long will it need to last?” The reality is that most retirees find their life expectancy increases as they get older. ‘Longevity literacy’ or ‘longevity awareness’ is an understanding of how long people tend to live in retirement. Improving longevity awareness can improve member decision-making.

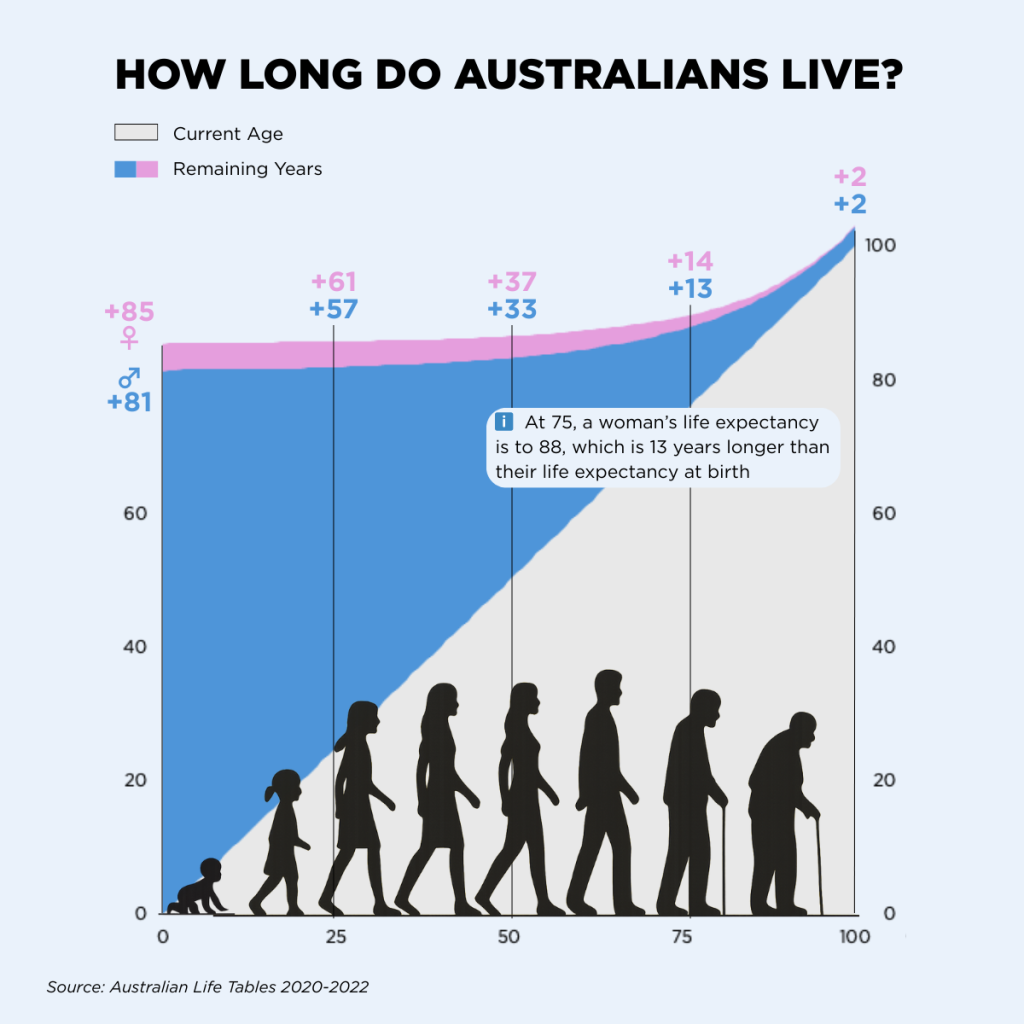

The chart above indicates that life expectancy at a given age is not a single number. Around half of retirees will live beyond the so-called “average” life expectancy, with a significant proportion living well into their late 80s and 90s.

It also illustrates that as you age, your life expectancy actually increases. Each birthday you reach means you’ve survived the risks of earlier years, and your odds of living longer go up. For example, at 75, a woman’s life expectancy is to 88, which is 13 years longer than their life expectancy at birth.

This highlights why ‘average life expectancy’ is a dangerous planning anchor. It also underscores why superannuation funds must help members plan for the real risk of outliving their savings.

Why Longevity Risk Matters for Member Outcomes

Understanding lifespan uncertainty is crucial for retirement planning success. From a member’s perspective, running out of money in their later years is one of the greatest retirement fears. Yet retirement planning models often rely on averages, understating the risk of living longer. The result: members either spend too cautiously and undershoot their lifestyle potential, or they spend too freely and risk hardship in later life.

Superannuation funds are uniquely positioned to help members avoid these poor outcomes by:

- Educating members that retirement may last 25–30 years, not just the ‘average’ lifespan.

- Equipping members with tools and strategies that factor in longevity risk.

- Encouraging members to balance flexible access to their savings with products that provide income for life.

The Regulatory Context: Retirement Income Covenant

The Retirement Income Covenant requires trustees to have a strategy to assist members in managing the expected risks of retirement, including longevity risk. This isn’t just a compliance exercise–it’s an opportunity to embed longevity awareness into advice, guidance, and communications so members make better decisions.

Funds that can demonstrate to APRA and ASIC how they are equipping members to manage these risks will be well placed to meet both regulatory expectations and member needs. Practical demonstrations include:

- Interactive calculators that show the full distribution of life expectancy or suggest a planning age that has a high probability of covering each person’s total potential lifespan.

- Clear documentation of how longevity risk is addressed in retirement income strategies

- Evidence of member engagement with longevity planning tools and education

- Product innovations that help members manage lifespan uncertainty

From Education to Action

Improving member outcomes on longevity requires more than risk warnings. It calls for engagement. Practical steps include:

- Interactive tools: Giving members access to calculators that consider the full distribution of life expectancy, not just the average.

- Personalised communication: Explaining the trade-offs between account-based pensions, lifetime income products, and Age Pension interactions in member-friendly terms.

- Decision support at key milestones: Integrating longevity planning into pre-retirement seminars, advice channels, and retirement transition pathways.

- Framing around lifestyle outcomes: Positioning income strategies in terms of maintaining dignity, freedom, and confidence in later life.

The Role of Funds: Supporting Confidence and Security

When members feel confident they won’t run out of money, they are more likely to enjoy their retirement and use their savings purposefully. Conversely, uncertainty about how long their money needs to last often leads to overly cautious spending, undermining retirement wellbeing.

By helping members understand and plan for longevity risk, trustees can:

- Increase trust and engagement.

- Deliver better alignment with the Covenant.

- Support measurable improvements in retirement adequacy.

This represents both a regulatory imperative and a competitive opportunity.

Call to Action

A practical way to start the longevity conversation is through tools that bring the issue to life for members. The Optimum Pensions Lifespan Calculator helps members get a more personalised estimate of life expectancy, sparking a more informed and realistic conversation about retirement income planning.

👉 Try the calculator here: Optimum Pensions Lifespan Calculator

👉 Learn more about starting the conversation: The Longevity Conversation

Closing Thought

Longevity risk is not just a technical challenge for actuaries or product designers. It is central to delivering better member outcomes in retirement. For funds, addressing it directly, through education, tools, advice, and product solutions, is both a regulatory requirement and a powerful way to improve the retirement confidence of members.