Navigating Uncertainty: The Role of Assumptions in Retirement Planning Tools

The unpredictability of life expectancy creates a significant risk when trying to estimate how long savings need to last, leading to potential shortfalls or unnecessarily conservative spending. In this context, retirement planning tools play a crucial role by offering projections based on critical assumptions, particularly about future life span. The accuracy of these assumptions is vital, as they provide the foundation for determining how much to save, when to retire, and how to manage finances throughout retirement.

Regulatory and Industry Guidance

The only regulatory guidance regarding retirement planning calculators are Regulatory Guide 276 Superannuation forecasts: Calculators and retirement estimates (RG 276) and ASIC (Superannuation Calculators and Retirement Estimates) Instrument 2022/603. Together, they set out conditions under which superannuation forecasts can be provided without an Australian Financial Services Licence.

On releasing these documents, then ASIC Commissioner Danielle Press said, ‘Superannuation calculators and retirement estimates are important tools that can help consumers engage with their superannuation, especially as they approach retirement”. According to RG 276, ASIC expects “providers of superannuation forecasts to provide these forecasts in a way that helps users think about their income in retirement” and “to present forecasts in a consumer-centric way that puts the needs of the user first”.

RG 276 sets out standard default assumptions for key variables like investment returns, inflation, and wage growth. When it comes to future lifespan, providers must, by default, assume that the drawdown period ends on the later of:

- the member reaching 92 years of age; and

- five years after the start of the drawdown period.

ASIC says that age 92 takes into account several factors, including life expectancy at retirement and future mortality improvements.

The Actuaries Institute has a couple of useful publications:

- Good Practice Principles for Retirement Modelling Technical Paper designed to uplift industry standards by encouraging good practice across retirement models developed in Australia; and

- Research Note 1: The Importance of Accurate Life Expectancy Calculations in Retirement Advice.

The Technical Paper recommends ten good practice principles to encourage good practice across retirement models developed in Australia. When it comes to the payment period or longevity/mortality basis, the paper recommends considering the following questions:

- How is the payment period determined?

- What is the longevity/mortality basis?

- Whether personal health is recognised?

- Have mortality improvements been allowed for? What basis?

The Research Note warns that methodologies used by superannuation funds and Australian Financial Services licensees have shown that many retirement calculation tools may not always reflect best practices regarding allowing for how long people live. It recommends that, as a minimum, providers calculate life expectancy using the Australian Government Actuary’s (AGA) published mortality tables as follows:

- Refer to the most recent Australian Life Table (currently 2015-17, and the AGA is due to publish new tables towards the end of the year) www.aga.gov.au/publications/#life_tables

- Choose an appropriate mortality improvement table – which allows for estimated ongoing improvements in life expectancy.

The note also recommends that superannuation funds and Australian Financial Services licensees:

- Include the age of both spouses if the household is a couple.

- Show results in a way that includes the range of possible lifespan that the individual or couple may experience.

The critical component: understanding how long to plan for

Our recent article, The Missing Piece: Longevity Awareness and Your Retirement Plan, emphasised the importance of longevity awareness in retirement planning. It highlighted that many Australians underestimate their life expectancy, which can lead to financial shortfalls.

Superannuation funds and financial planners play a critical role in helping clients define a realistic retirement time horizon rather than relying solely on average life expectancy figures. While population averages can provide a general guideline, they may not reflect individual circumstances such as health, lifestyle, and family history. A personalised approach is essential because underestimating how long a client will live could result in depleted savings while overestimating could lead to overly cautious spending and a diminished quality of life in retirement. By carefully assessing each client’s unique situation and regularly revisiting these projections, financial planners can create tailored strategies that offer greater security and flexibility for managing long-term retirement needs.

Longevity literacy helps retirees make informed decisions about how long their savings need to last. Tools like the Optimum Pensions Lifespan Calculator assist in estimating a realistic retirement horizon, considering personal factors. Improving longevity literacy not only reduces the risk of outliving savings but also enhances overall retirement security and confidence.

Canadian Projection Assumption Guidelines for Financial Planners

The Institute of Financial Planning and FP Canada Standards Council jointly publish the Projection Assumption Guidelines to help financial planners make realistic financial projections. Recognising the importance of the planning horizon, these guidelines recommend financial planners assume a projection period for clients where the probability of outliving their capital is no more than 25%. The rationale is that forecasting a longer projection period offers protection from future improvements in mortality and accounts for the greatest financial risk to an individual: longevity risk.

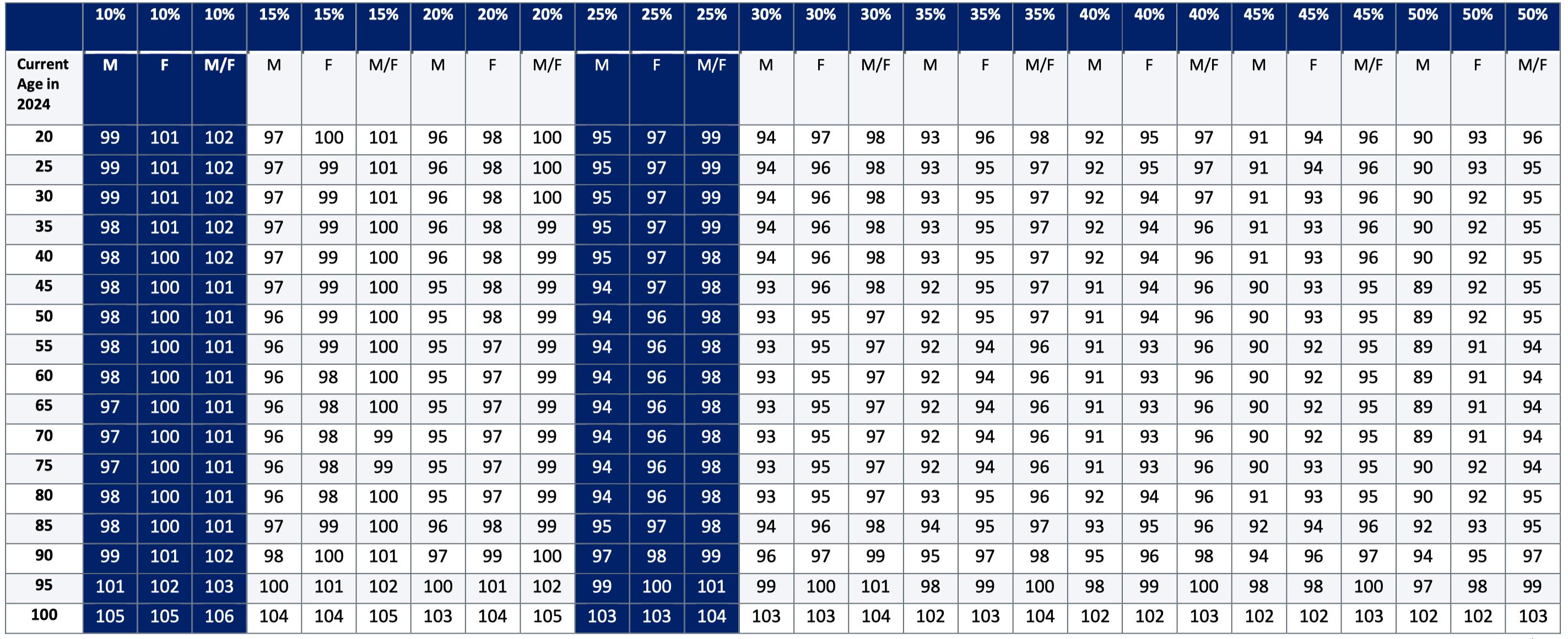

To help financial planners, the guidelines include a probability of survival table (see Table 1) and encourages financial planners to develop sensitivity analyses related to mortality (e.g., +/- 5 years), given the dramatic effects that may result when the projection period is changed by a relatively small number of years.

Table 1: Probability of Survival Table

We spoke to Martin Dupras, one of the authors of the guidelines. He said that they are designed to protect both advisor and consumer. Prior to the introduction of the guidelines, financial planners used life expectancy. When FP Canada demonstrated that this means that the retirement plans they prepare have a 50% of not working, Canadian financial planners have generally adopted the guidelines.

Retiring with confidence

Retirement planning calculators are essential tools for superannuation funds and financial planners, helping individuals visualise their financial futures and make informed decisions. However, their effectiveness relies on using appropriate assumptions and understanding their limitations.

Effectively communicating the results of retirement planning calculators is crucial for helping individuals make informed decisions about their financial futures. By moving beyond single-point estimates and embracing methods that convey the range and variability of potential outcomes, superannuation funds can provide individuals with a more realistic and useful understanding of their retirement prospects.

By leveraging these tools wisely, educating individuals about their use, and adopting industry best practices, superannuation funds and financial planners can enhance the retirement planning process, ultimately leading to better outcomes for their individuals. This approach not only satisfies legal obligations but also reinforces trust in the retirement planning process and helps build a more financially secure future for all.

####

Authors: David Orford & Stephen Huppert[/vc_column_text][vc_column_text]***

Optimum Pensions was launched in 2017 with a single mission – to help Australians lead a comfortable retirement. The Optimum Pensions innovative retirement income solutions are specifically developed to address longevity risk and provide greater peace of mind for all retirees; no matter how long they live.

The Optimum Pensions, award-winning LifeSpan Calculator builds confidence around personal life expectancy and retirees’ possible retirement planning horizon.